[SID2022] NANOSYS Booth in Display Week

NANOSYS는 디스플레이용 퀀텀 닷을 생산하는 기업입니다.

Quantum Dot Enhancement Film(QDEF) 빛을 더 밝고 화려하게 만드는 광학 필름입니다.

다양한 기업들의 QD 디스플레이를 비교할 수 있는 공간이 마련되어 있었습니다.

NANOSYS는 디스플레이용 퀀텀 닷을 생산하는 기업입니다.

Quantum Dot Enhancement Film(QDEF) 빛을 더 밝고 화려하게 만드는 광학 필름입니다.

다양한 기업들의 QD 디스플레이를 비교할 수 있는 공간이 마련되어 있었습니다.

■ Investment cost comparison and analysis for WRGB OLED, solution processed OLED and QD-OLED

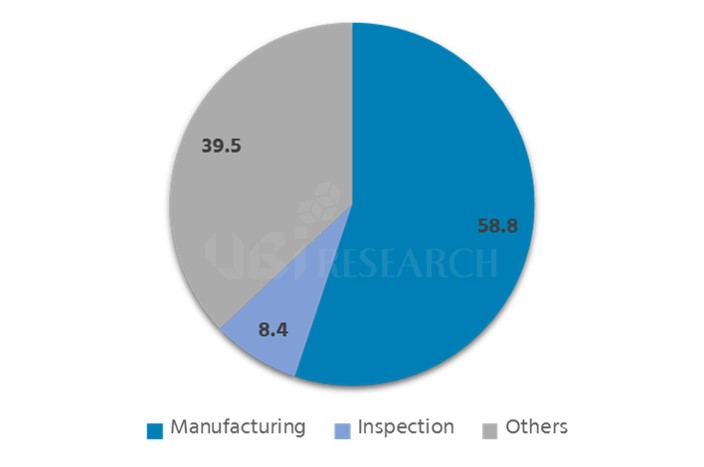

■ Total OLED process equipment is expected to form a market of US$ 58.8 billion from 2018 to 2022, and inspection equipment market is estimated as US$ 8.4 billion

In the premium TV market, the market share of OLED TVs is steadily rising, and the number of OLED TV camps is gradually increasing. OLED TV adopts color filter to WRGB OLED, and currently LG Display only mass produces the OLED panels.

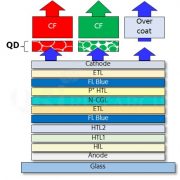

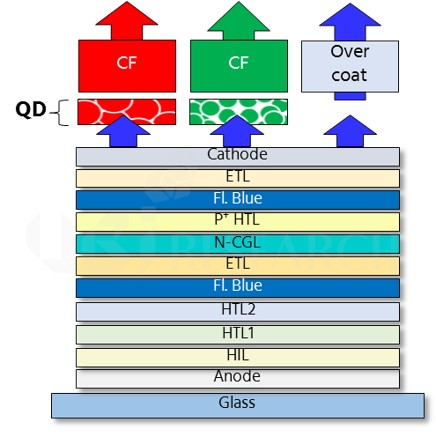

On the other hand, Samsung Display is developing QD-OLED (blue OLED + quantum dot color filter) to compete with WRGB OLED in the premium TV market. Blue OLED is a technology in which the blue light emitted from OLED passes through a quantum dot layer and a color filter to represent red and green colors.

<Expected structure of QD-OLED>

UBI Research analyzed the structure and investment amount of WRGB OLED and QD-OLED, which are the latest issues, in the‘AMOLED Manufacturing and Inspection Equipment Industry Report’ published on June 6. In addition, the investment amount of the solution process OLED, which has got the industry attention due to its possible implementation of real RGB in large-area OLED, is also analyzed and compared.

As a result of analyzing the equipment investment cost based on the 8th generation 26K, the QD-OLED investment cost is 3% higher than WRGB OLED and the investment cost of solution process OLED is 19% less than that of WRGB OLED.

In the QD-OLED investment cost, it is reflected that QD color filter is separately formed and its laminating process is added. For the analysis of solution processed OLED investment cost, color filter is excluded and ink-jet printer is applied instead of deposition equipment.

In addition, the report forecasts the overall OLED equipment market from 2018 to 2022. The total OLED overall equipment market is expected to reach US$ 106.7 billion from 2018 to 2022. The market for process equipment is projected as US$ 58.8 billion and inspection equipment market is to be US$ 8.4 billion.

최근 premium TV 시장은 OLED TV의 점유율이 지속적으로 상승하고 있으며 OLED TV 진영도 꾸준히 증가하고 있는 추세다. OLED TV는 WRGB OLED에 color filter를 적용한 구조로써, 현재 LG Display만이 유일하게 OLED panel을 양산하고 있다.

이에 Samsung Display에서는 premium TV 시장에서 WRGB OLED에 대항하기 위해 blue OLED + quantum dot color filter(이하 QD-OLED)를 개발하고 있는 것으로 알려졌다. Blue OLED는 OLED에서 발광 된 청색광이 quantum dot층과 color filter를 통과해 red와 green 색을 나타내는 기술이다.

<QD-OLED 예상 구조>

유비리서치는 지난 6일 발간한 ‘AMOLED Manufacturing and Inspection Equipment Industry Report’에서 최근 이슈가 되고 있는 WRGB OLED와 QD-OLED의 구조와 투자 금액을 분석했다. 뿐만 아니라, 대면적 OLED에서 real RGB를 구현할 수 있어 주목받고 있는 solution process OLED의 투자 금액도 함께 분석하여 비교했다.

8세대 26K 기준으로 장비 신규 투자비를 분석한 결과, QD-OLED 투자비는 WRGB OLED에 비해 3%가 많고 solution process OLED는 WRGB OLED에 비해 19% 적은 것으로 조사되었다.

QD-OLED 투자비에서는 QD color filter가 따로 형성되고 이를 합착하는 공정이 추가된 내용이 반영되었으며, solution process OLED 투자비에서는 color filter가 제거되고 증착 장비 대신 ink-jet printer가 투입된 내용이 반영되었다.

이 밖에 본 보고서에서는 2018년부터 2022년까지 OLED 전체 장비 시장도 예상하였다. 2018년부터 2022년까지 OLED 전체 장비 시장은 US$ 106.7 billion을 형성할 것으로 전망되며, 공정 장비는 그 중 US$ 58.8 billion, 검사 장비는 US$ 8.4 billion의 시장을 형성할 것으로 예상된다.

<2018년~2022년 장비별 전체 시장 점유율 전망>

Samsung Electronics reported sales of KRW 62.05 trillion and operating profit of KRW 14.53 trillion through the conference call of the third quarter in 2017, and the display business recorded sales of KRW 8.28 trillion and operating profit of KRW 0.97 trillion. Display business sales increased 7.4% compared to the previous quarter and 17.3% compared to the previous year, but operating profit of 1 trillion fell with a decrease of 43.3% of the previous quarter and 4.9% the previous year. OLED sales are shown to occupy 60% of the display industry.

According to Samsung Electronics, in the 3rd quarter of 2017, main customers of OLED have increased through the launch of new flagship products focused on flexible products. However, its performance has decreased than the previous quarter due to factors such as increased costs of new OLED lines initial ramp-ups, and intensified price competition between rigid OLEDs and LCD panels.

Samsung Electronics plans to increase supply of flexible products in OLED in the 4th quarter, and expand sales of rigid OLED products to secure profitability. In the LCD industry, there are off-seasons and excess supplies resulting to supply and demand imbalance, but profitability is to be secured by strengthening yield and cost activities and expanding sales portion of high value-added products such as UHD, large-format, and QD.

In 2018, OLEDs are expected to become the mainstream in the mobile display market, with expectations that flexible panel dominance will be particularly strong in the high-end product line. Samsung Electronics said it plans to develop a system to meet the flexible demand of major smartphone manufacturers and improve earnings by securing differentiated technologies.

In 2018, the LCD market may continue to expand in China and intensify competition among companies, but trend of large-sized and high-resolution TVs are expected to continue. Samsung Electronics states it will strengthen its strategic partnership with its customers and concentrate on improving profitability by promoting sales of high value-added products such as UHD, large format, QD, and frameless products.

Samsung Electronics sold 97 million mobile phones and 6 million tablets in the 3rd quarter of 2017. Mobile phone sales in the 4th quarter are expected to decline Quarter on Quarter, but tablet sales are expected to increase QoQ. TV sales reached a record around 10 million units, and sales in the 4th quarter were expected to rise to mid-30%.

10.4 trillion was invested in facility during the 3rd quarter of Samsung Electronics, of which 2.7 trillion was invested in display. Displays are reported to have additional production lines to meet customer demands for flexible OLED panel.

CEO Chang-Hoon Lee of Samsung Display said, “In the case of small and medium-sized OLEDs, we are planning to apply it to AR, VR, foldable, and automotive industry.” Also, “In Automotives, OLEDs are focused on energy efficiency, design differentiation, and black image quality which is critical to driver safety, in preparation with client company cooperation.” Additionally, “Foldable is constantly being researched and developed in line with customer demand, and is centered on enhancing the level of perfection demanded by the market and customers. We will work with our clients to prepare these for mass production desired by our customers.”

삼성전자는 31일 진행된 2017년 3분기 실적 컨퍼런스콜을 통해 매출 62.05조원, 영업이익 14.53조원을 기록했으며, 이 중 디스플레이 사업에서 매출 8.28조원, 영업이익 0.97조원을 기록했다고 밝혔다. 디스플레이 사업 매출은 전분기 대비 7.4%, 전년 동기 대비 17.3% 증가했지만, 영업이익은 1조원대가 무너지며 전분기 대비 43.3%, 전년 동기 대비 4.9% 감소했다. 디스플레이 사업에서 OLED 매출은 60% 후반의 비중을 차지했다고 밝혔다.

삼성전자에 따르면 2017년 3분기에는 OLED 부문에서 주요 고객사의 플래그십 신제품 출시로 flexible 제품을 중심으로 매출이 증가했다. 하지만 신규 OLED 라인 초기 ramp-up에 따른 비용 증가, rigid OLED와 LCD 패널 간의 가격 경쟁 심화 등의 영향으로 전분기 대비 실적이 감소했다고 설명했다. LCD 부문은 주요 고객의 재고 조정 등에 의해 판가 하락 영향으로 실적이 약화되었고 밝혔다.

삼성전자는 4분기 OLED 부문에서 flexible 제품의 생산성을 높여 공급을 본격적으로 확대하고, rigid OLED 제품 판매를 확대해 수익성을 확보할 계획이다. LCD 부문의 경우 계절적 비수기와 업계의 공급 초과 상황이 지속되어 수급 불균형의 우려가 있으나, 수율과 원가 개선 활동을 강화하고, UHD, 대형, QD 등의 고부가 제품 판매 비중을 확대해 수익성 확보에 주력할 방침이라고 밝혔다.

2018년에 OLED는 모바일 디스플레이 시장에서 mainstream이 될 것으로 기대되며, 특히 high-end 제품군에서 flexible 패널의 지배력 강화가 전망된다고 밝혔다. 삼성전자는 주요 스마트폰 업체들의 flexible 수요에 적기 대응할 수 있는 시스템을 구축하고, 차별화된 기술 확보를 통해 실적 개선을 추진할 계획이라고 설명했다.

2018년에 LCD 시장은 중국의 생산량 확대가 지속되고 업체간 경쟁도 심화되지만, TV의 대형화와 고해상도 트렌드 또한 지속될 것으로 전망된다고 밝혔다. 삼성전자는 고객사와의 전략적 파트너십을 견고히 하고, UHD, 대형, QD, frameless 등 고부가 제품과 디자인 차별화 제품의 판매 확대를 추진해 수익성 제고에 집중할 방침이라고 밝혔다.

삼성전자는 2017년 3분기에 휴대폰 9,700만 대, 태블릿 600만 대의 판매량을 기록했다. 4분기 휴대폰 판매량은 전분기 대비 감소할 것으로 예상하지만, 태블릿 판매량은 전분기 대비 증가할 전망이라고 밝혔다. TV의 판매량은 약 1,000만대를 기록했으며, 4분기 판매량은 30% 중반대의 상승을 예상했다.

삼성전자의 3분기 시설 투자는 총 10.4조원이 집행되었고, 이 중 디스플레이에 2.7조원이 투자됐다. 디스플레이의 경우는 flexible OLED 패널 고객 수요에 대응하기 위한 생산라인 증설 투자가 진행중이라고 설명했다.

삼성디스플레이 이창훈 상무는 “중소형 OLED의 경우 현재 주력인 스마트폰 외에도 AR, VR, foldable, automotive 등에 확대 적용할 예정”이라고 설명했다. 이어 “Automotive에서는 OLED가 에너지 효율, 디자인 차별화, 운전자의 안전에 중요한 블랙 화질 구현 등의 장점으로 관심이 집중되고 있어 앞으로 고객사와 협력을 통해 준비하겠다”고 설명했다. 또한, “Foldable은 고객 수요에 맞춰 지속적으로 연구, 개발 중이며 시장과 고객이 원하는 수준의 완성도 제고에 중심을 두고 있다. 고객사와 협력을 통해 고객이 원하는 시점에 양산 가능하도록 준비하겠다”고 덧붙였다.

Currently in the market of premium TV, OLED TV and QD- LCD industries are highly competitive.

QD vision with Nanosis and SID 2016 and IFA 2016 also emphasized quality of TV with QD material included comparing quality of OLED TV. Against this, LG Display joined the completion by emphasizing quality of OLED TV as an ideal display for HDR with comparison between QD-LCD and OLED in IFA 2016 with from SID 2016,

In current large surfaced TV market, LCD TV is taking overwhelmingly large share in distributed market while OLED TV gradually is growing large share in premium market.

In looking into strategies of each industry, large surfaced OLED is developing solution process OLED in order to achieve broader market share with from premium model to distributed model. To overcome weakness compared to OLED, LCD TV industry progressively use QD material with the final goal of development of QLED technology

As a competition in premium TV market gradually extends to entire area of TV market, present condition and possibility of market entry with solution process OLED and QLED is one of major interest.

For this matter, there is seminar host by Ubi Industrial Research with the theme of “analysis in possibility of market entry with QLED and Solution process OLED” in Medium sized business center, Yeouido, October 14th and will be discussing present market industry of large surfaced TV and panel and also will be dealing with present condition and issue of QLED and Solution process OLED, and future possibility of market entry.

Choong-Hoon Lee, president of Ubi Industrial Research, will suggest future direction of OLED industry with analysis of present condition and possibility of market entry in OLED and QLED.

Sung-Jin Jung, head of department of Du Pont, will be discussing the timing of market entry of solution process OLED with the demonstration of soluble OLED material, the essential part of solution process OLED, including present trend and up to date developmental technique

Professor Chang-Hee Lee and senior researcher Ji-won Bang from Korean Institute of Ceramic Engineering and Technology(KICET) will be discussing about advantage and developmental issue of Quantum dot material and direction of future development.

The seminar attracts attention in terms of providing an opportunity to share and discuss regarding issue through media and exhibition with technological and market perspectives of Ubi Industrial Research and share opinions and future possibility.

For registration and any inquiry, please contact to Hana Oh (hanaoh@ubiresearch.co.kr, 02 577 4940) from Ubi Industrial Research.

출처= SDC

강현주 / jjoo@olednet.com

오는 2017년까지 삼성디스플레이( SDC ) OLED 설비투자 규모는 애플, 삼성전자 IM (무선사업부) 등 2개의 고객으로만 15조원에 이를 것이라는 전망이 나왔다.

현대증권 김동원 애널리스트는 24일 이같이 전망하며 이로 인해 6세대 기준의 삼성 플렉서블 OLED 생산능력(캐파)은 2015년 월5만장에서 ‘16년 18만장, ‘17년 27만장으로 추정된다고 내다봤다.

김 애널리스트에 따르면 OLED 장비업체들은 상반기 신규수주가 3분기 실적부터 본격 반영되기 시작해 하반기에는 시장예상을 상회할 가능성이 높아 보인다. 이는 OLED 장비업체의 하반기 실적이 ‘16년 연간 실적의 70~90%를 차지하는 뚜렷한 상저하고 이익패턴이 예상되기 때문이다. 따라서 테라세미콘, AP시스템, 에스에프에이, 동아엘텍 등 OLED 장비업체들은 하반기 어닝 서프라이즈가 기대된다는 게 그의 설명이다.

이와 함께 김동원 애널리스트는 올해 삼성전자의 퀀텀닷 TV 출하량이 350만대, 전년대비 250% 증가할 것으로 예상했다. 이는 퀀텀닷 (QD) 소재가 화면 사이즈에 관계없이 대화면 LCD TV에 쉽게 적용할 수 있고, 잉크젯 프린팅 공정 및 화이트 OLED (WOLED)에 접목해 향후 OLED TV 시장에서 QD OLED TV로 제품 차별화가 가능하며, 장기적으로 QLED (QD LED) TV 구현도 시도해 볼 수 있어 폭 넓은 확장성을 보유하고 있기 때문이다.

특히 2015년 100만대 불과했던 삼성전자 퀀텀닷 TV 출하량은 2016년, 17년에 전년대비 각각 250%, 140% 증가한 350만대 (상반기 100만대, 하반기 250만대), 840만대로 추정되어 삼성전자 전체 TV에서 차지하는 퀀텀닷 TV 출하비중은 2015년 2%에서 2016년, 17년에 각각 7%, 18%까지 확대될 전망이다. 이에 따라 삼성전자 퀀텀닷 TV에 소재 및 인버터의 독과점 공급권을 확보한 한솔케미칼, 한솔테크닉스 하반기 실적은 큰 폭 개선이 기대된다.

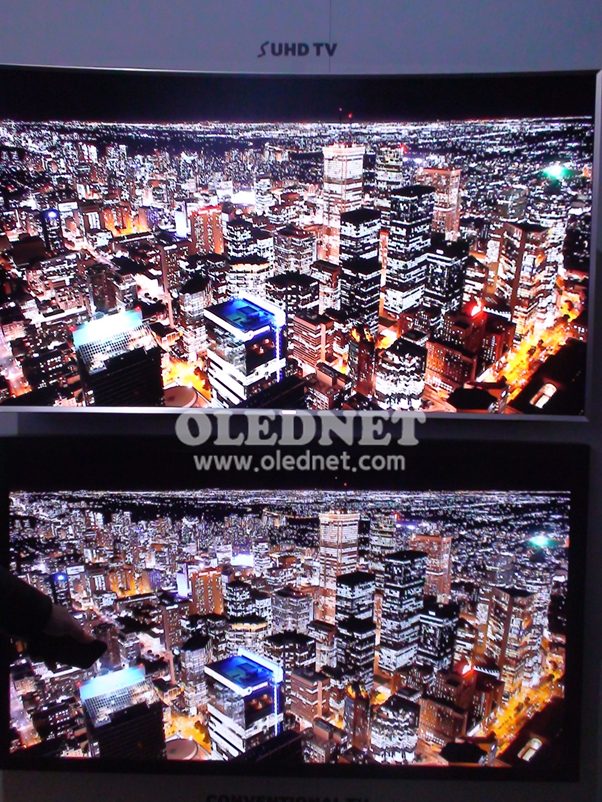

LCD TV에 또 한번 대 혁신이 생겼다. Quantum dot(QD)을 사용한 LED BLU로서 LCD TV 화질은 이제껏 누구도 상상할 수 없는 궁극의 경지까지 도달했다.

CES2015에서 삼성전자를 비롯하여 LG전자, Sony, Sharp, TCL, Haier 등 TV 세트 업체들이 QD-BLU LCD TV를 공개했다. QD-LED로 인해 색재현율은 NTSC 110%까지 모두 도달하였으며, HDR(high dynamic range) 기술로서 휘도와 명암비가 이제까지의 LCD 패널에서는 볼 수 없었던 화려한 화질을 얻을 수 되었다. 기존 LCD TV는 명암비가 분명하게 나타나는 야경을 화면에 나타내는 전시는 거의 볼 수 없었으나 CES2015에서 삼성전자는 SUHD TV(상)와 기존 LCD TV와의 명암비를 직접 비교하는 전시로서 LCD TV가 얼마나 좋아졌는지를 보여주었다.

또한 외관에서는 curved와 10mm이하의 박형 디자인으로 기존 LCD TV와는 확연히 차이 나는 변화를 보여주었다. Wide color LCD는 시야각마저도 거의 자발광 수준에 도달했다.

도대체 LCD TV는 어디까지 진화할까?

이번 CES2015에서 답이 나왔다.

OLED TV까지이다.

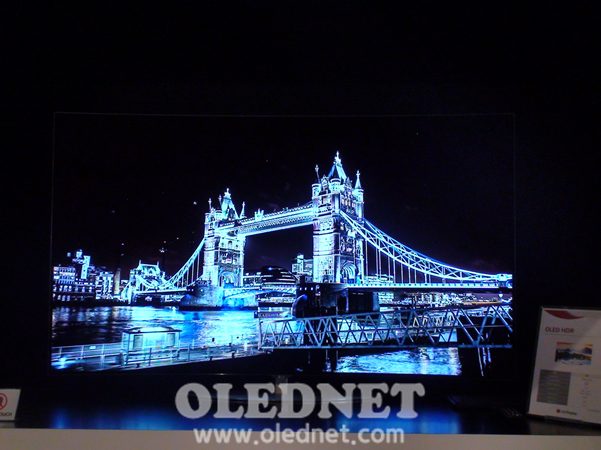

LG, 65inch OLED TV

OLED panel을 생산할 수 있는 업체는 전 세계에서 LG디스플레이가 유일하며, 현재 시점에서 OLED TV를 대량 생산할 수 있는 업체는 LG전자뿐이다.

OLED 패널이 가지고 있는 색재현성과 명암비, 응답속도, 시야각, 두께 등은 삼성전자가 생산하는 smart phone Galaxy series에서 이미 LCD 보다 월등히 우수함이 증명되었다. 따라서 OLED TV를 만들 수 없는 TV 업체들의 생존 수단은 OLED 패널을 대량으로 수급 할 수 있을 때까지는 어떻게 하든지 LCD TV를 최대한 OLED TV와 유사하게 만드는 것이다.

이번 CES2015에는 LCD TV가 할 수 있는 모든 기술이 총 동원되어 LG전자의 OLED TV 따라가기에 동원되었다. LCD TV는 색재현성과 시야각, 두께, 두꺼워짐에도 불구하고 휘어놓은 curved 디자인으로 OLED TV와 최대한 근접해졌다. 특히 HDR 기술로서 향상 시킨 명암비는 설명이 없으면 OLED TV로 착각할 정도로 좋아졌다. 하지만 LCD는 LCD이고 OLED는 역시 OLED이다. 흉내는 낼 수 있어도 같아 질 수는 없다.

OLED TV가 나옴에 따라 LCD TV가 다시 한번 변신하는 계기가 마련된 것은 TV 역사에서 바람직한 경쟁 사례로 길이 남을 것이다.